Hybrid Agent

Most consumers have never heard of the term Hybrid Agent. It sounds really fancy, but at the end of the day, all it means is someone who’s about to save you a lot of time and money on your real estate transaction. A Hybrid Agent is a Real Estate Agent and a Licensed Mortgage Loan Officer wrapped up in the same person. An agent who legally is licensed to practice both sides of your real estate transaction. There are several reasons that you would want to use a Hybrid Agent to help you out with your real estate transaction. I’ll be sure to cover them here.

Most consumers have never heard of the term Hybrid Agent. It sounds really fancy, but at the end of the day, all it means is someone who’s about to save you a lot of time and money on your real estate transaction. A Hybrid Agent is a Real Estate Agent and a Licensed Mortgage Loan Officer wrapped up in the same person. An agent who legally is licensed to practice both sides of your real estate transaction. There are several reasons that you would want to use a Hybrid Agent to help you out with your real estate transaction. I’ll be sure to cover them here.

Hybrid Agent Rebate

As a hybrid Agent, I’m able to pay your closing costs. Because I’ll be working on both sides of the transaction, I’m going to be paid for each side. When that happens, I’m able to apply a portion of the real estate commission towards your closing costs. In most cases, we’re able to go up to 50% of the real estate commission. THAT’S HUGE! Imagine buying a $300,000 home and getting $4,500 dollars towards your closing costs from your Real Estate Agent.

It’s almost too good to be true. In fact, I encourage you to just pick up the phone, call a local realtor and ask them for half their commission to go towards your closing cost. Chances are they are going to hang up on you. It’s a lot to ask of your average realtor as they work really hard and aren’t willing to give up those funds. However, since we get paid twice it’s a lot easier for us to provide that value to our clients.

It’s almost too good to be true. In fact, I encourage you to just pick up the phone, call a local realtor and ask them for half their commission to go towards your closing cost. Chances are they are going to hang up on you. It’s a lot to ask of your average realtor as they work really hard and aren’t willing to give up those funds. However, since we get paid twice it’s a lot easier for us to provide that value to our clients.

Having a Loan Officer that understands the real estate side helps as well. The $4,500 that we’re giving you as a realtor credit can be used to make sure you’ve got the best loan as well. You can do a number of things with that money. We would analyze your situation and see if we needed to get rid of the PMI by buying it out or buying down the interest rate… or both! If you wanted to just bring less money to closing we could also just apply the rebate towards that. What would you use your savings towards?

Hybrid Agent also saves you time

In your typical real estate transaction, you have to work with two different people. You’ll have a set of questions for the realtor and you’ll have questions for the lender. Personally, I’ve been in the position when a client asks me a question on the real estate side that I’m not the realtor on. To keep professional courtesy, I have to defer to their real estate agent.

However, I’ve had clients ask me these questions when I was operating as a hybrid agent and they got their answers immediately. In fact, I love the idea that I can be on a home showing and work up loan numbers for that particular home on the spot. As a real estate agent and mortgage loan officer, I have access to all the information. Imagine being on a showing and knowing exactly what the house is going to cost you. Instead of watching your agent, get on the phone to call their lender and trying to get numbers together. It helps you make a decision on putting an offer in on your dream home on the spot. Through, my years of experience as a loan officer. People don’t really get excited about the mortgage loan. The excitement is house shopping. I can assure you it’s a much easier way of doing business and it’s much smarter as well.

Hybrid Agent Future Options

This is probably one of the most important pieces of using a Hybrid Agent. When you’re purchasing a home, it’s not just your living quarters. For most people, it’s your largest financial investment. With that being said, it’ll need to be managed as such. I’m sure you’ve heard on the news that the fed has lowered interest rates or the housing markets have increased.

These are chances to better your financial position with your mortgage. You could refinance your mortgage for a lower payment. You could do home upgrades by taking equity out of your home to maybe remodel. You could also possibly pull cash out of your equity for any other projects that you may have.

Equity is the difference in what you owe vs. what it’s worth. Imagine you have a home that has a market value of $300,000, but you only owe $150,000. In this particular scenario, you have $150,000 in equity in your home. THIS IS WHY PEOPLE SAY IF YOU’RE NOT BUYING A HOME YOU’RE THROWING AWAY MONEY.

You gain access to that equity when you refinance or you sell the home. As a Hybrid Agent, I would have all the information about your property and your current loan numbers. We would be in contact with you throughout your homeownership to make sure you’re in the best financial position possible. It’s more than just a mortgage loan. It’s Mortgage Planning. We’re going to make sure you’ve always got the best loan and you’re maximizing your equity position.

Hybrid Agent- Lending Difference

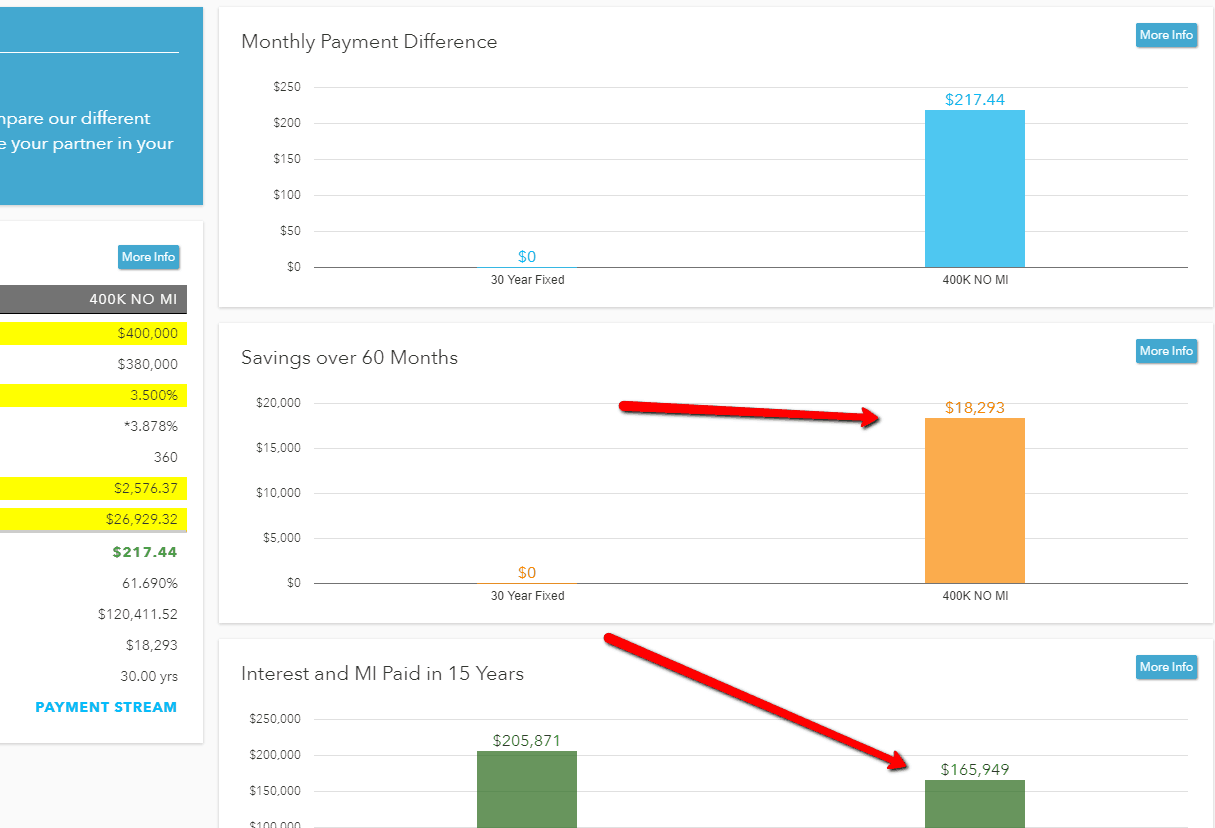

As a hybrid agent, the financial side is huge. I use a program called mortgage coach that will show you the difference in using a Hybrid Agent vs. A Traditional Realtor. When you see the numbers side by side, there is no doubt in my mind that you’ll choose to work with #hybridagent. It just makes sense.

As a hybrid agent, the financial side is huge. I use a program called mortgage coach that will show you the difference in using a Hybrid Agent vs. A Traditional Realtor. When you see the numbers side by side, there is no doubt in my mind that you’ll choose to work with #hybridagent. It just makes sense.

As you can see using a Hybrid Agent holds several advantages over a traditional Real Estate Agent. Here is one example of me saving a client over $30,000 because the loan was structured properly. They were able to save over 18K in the first 5 years of homeownership? Could you use an extra $18K in your bank account? Obviously, we’ll work up your personal total cost analysis to see exactly how much you’re going to save as well.

To get more information on the hybrid agent program and to start searching for homes. Check Out Our Hybrid Agent Page ==>